For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online.

The accounting equation And how it stays in balance

It gives an idea of the company’s overall financial position by ensuring that every transaction keeps the books balanced. On the other hand, the working capital formula focuses on short-term financial health by measuring liquidity and the company’s ability to meet its short-term obligations with the most liquid assets. The balance sheet is a more detailed reflection of the accounting equation. It records the assets, liabilities, and owner’s equity of a business at a specific time. Just like the accounting equation, it shows us that total assets equal total liabilities and owner’s equity. The purpose of this article is to consider the fundamentals of the accounting equation and to demonstrate how it works when applied to various transactions.

What Is The Double-Entry Bookkeeping Method?

The income statement is the financial statement that reports a company’s revenues and expenses and the resulting net income. While the balance sheet is concerned with one point in time, the income statement covers a time interval or period of time. The income statement will explain part of the change in the owner’s or stockholders’ equity during the time interval between two balance sheets. Valid financial transactions always result in a balanced accounting equation which is the fundamental characteristic of double entry accounting (i.e., every debit has a corresponding credit).

Equity

- However, modern financial operations like derivatives mergers or long-term contracts usually involve multiple layers of value and risk that cannot be captured by a simple equation.

- This straightforward relationship between assets, liabilities, and equity is considered to be the foundation of the double-entry accounting system.

- On 28 January, merchandise costing $5,500 are destroyed by fire.

- The 500 year-old accounting system where every transaction is recorded into at least two accounts.

However, a reduction in assets reduces both the asset and liability or equity side to keep the equation balanced. It’s telling us that creditors have priority over owners, in terms of satisfying their demands. While the basic accounting equation’s main goal is to show the financial position of the business.

Key Features of the Dual Aspect Concept

Because there are two or more accounts affected by every transaction, the accounting system is referred to as the double-entry accounting or bookkeeping system. Income and expenses relate to the entity’s financial performance. Individual transactions which result in income and expenses being recorded will ultimately result in a profit or loss for the period. The term capital includes the capital introduced by the business owner plus or minus any profits or losses made by the business.

Company

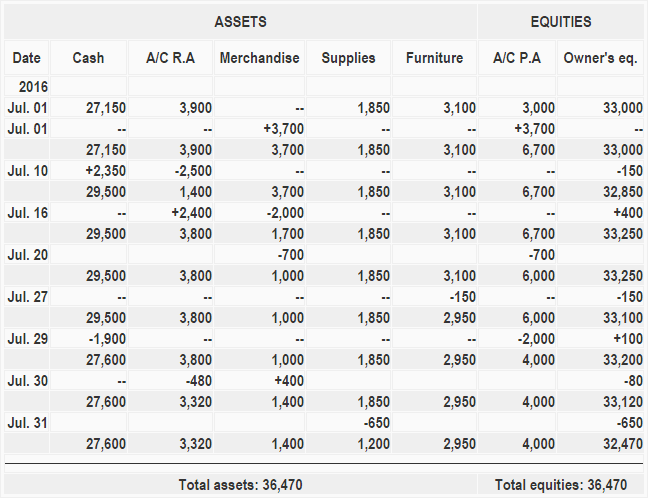

After recording these seven transactions, our accounts now look like this. We have all our assets listed on the debit side and all our liabilities and owner’s equity listed on the credit encumbrance definition side. Any changes in assets directly influence the accounting equation. When it increases, there must be a corresponding increase in either liabilities or equity to maintain the balance.

Now that we know the Debit side has decreased, we need to record the second side of the transaction that will keep the equation in balance. It will always be true as long as all transactions are appropriately accounted for and can never fail or be out of balance for any given entity. Accounting books, annual accounts, compulsory chartered accountants… Assets are the resources that the business owns, and from which the company is likely to benefit in the future. Metro Corporation collected a total of $5,000 on account from clients who owned money for services previously billed.

Liabilities refer to debts or obligations owed by the business. They are a particular amount owed to creditors of the business. Examples of liabilities include accounts payable, bank loans, and taxes. The accounting equation is also useful when considering how these assets will influence the company’s equity and overall financial strength when considering new investments. The ultimate goal is to ensure the investment adds value without disrupting the balance in the equation.

For instance, underestimating depreciation could make profits look higher than they actually are, which may mislead investors. On the other hand, overly cautious estimates could hurt a company’s profitability and future decisions. Many financial figures like asset values or bad debt provisions depend on personal judgment. These estimates can differ depending on the assumptions made by management, which might not always reflect reality. As a result, two companies might report the same type of transaction differently, leading to inconsistencies in financial reports. This guide will explore the accounting equation, its applications, some examples, and other crucial aspects.